Welcome to Contract for Deed Guys in Minnesota

If you’re considering contract for deed in Minnesota, one of the most important steps is understanding both the benefits and the risks before making a decision.

This type of agreement can provide a path to homeownership for buyers who cannot access traditional financing. At the same time, it comes with a structure that is different from a mortgage and requires careful evaluation.

This page breaks down the pros and cons of contract for deed in Minnesota in a clear, balanced way—so you can determine whether it fits your situation or if another path may be better.

Why Buyers in Minnesota Consider Contract for Deed

Buyers typically explore contract for deed because traditional financing is not always accessible or practical in the moment.

In Minnesota, this option is often considered by people who:

- Have difficulty qualifying for a mortgage

- Are self-employed or have non-traditional income

- Are recovering from past credit challenges

- Want to move forward with a home purchase sooner

Instead of waiting months or years to meet strict lending requirements, contract for deed creates a direct agreement between buyer and seller.

That said, choosing this route should not be based only on urgency. It should be based on a clear understanding of both the upside and the risks involved.

Pros of Contract for Deed in Minnesota

There are real advantages to this approach when it is structured properly and used in the right situation.

Flexibility

One of the biggest advantages of contract for deed is flexibility.

Because the agreement is negotiated directly between buyer and seller:

- Terms can sometimes be adjusted to fit the buyer’s situation

- Down payments may be more negotiable

- Payment structures can vary

This flexibility can make a difference for buyers who do not fit neatly into standard mortgage requirements.

However, flexibility depends entirely on the seller and the agreement—not all contracts will be favorable.

Access for Some Nontraditional Buyers

Contract for deed can open doors for buyers who might otherwise be locked out of the market.

This includes:

- Buyers with imperfect credit

- Buyers without long credit histories

- Buyers with inconsistent or self-employed income

Instead of being evaluated by a bank’s rigid criteria, buyers are evaluated directly by the seller, which can create more opportunities.

Potential Speed

Another advantage is speed.

Without the need for traditional underwriting, approval, and lender processes:

- Transactions can move faster

- Buyers may secure a property sooner

- There may be fewer delays compared to mortgage closings

For buyers trying to act quickly in a competitive market, this can be a meaningful benefit.

Cons of Contract for Deed in Minnesota

While there are benefits, there are also important risks that should not be overlooked.

Legal and Contract Risk

Contract for deed agreements are highly dependent on the written terms.

Unlike standardized mortgage contracts:

- Terms can vary significantly

- Some agreements may favor the seller heavily

- Key protections may not be as strong

This means buyers must fully understand what they are signing.

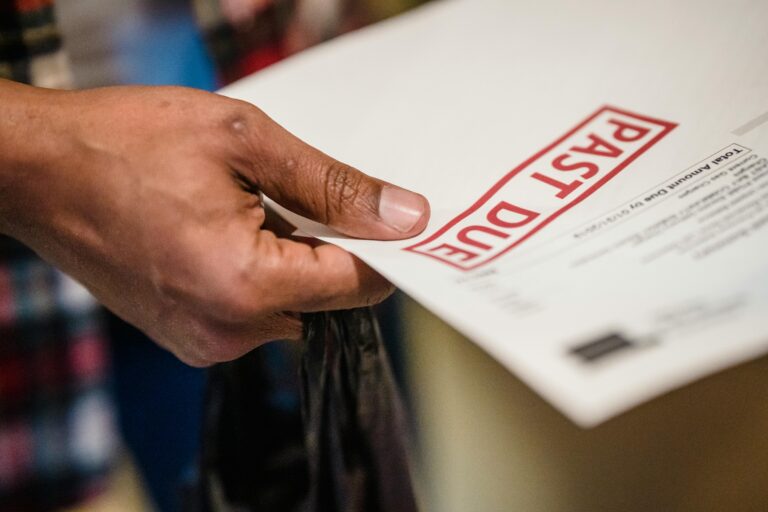

Loss Risk if Terms Are Not Met

One of the most serious risks is what happens if the buyer cannot meet the terms of the agreement.

If payments are missed or obligations are not fulfilled:

- The seller may initiate cancellation procedures

- The buyer could lose their position in the property

- Payments made may not be fully recoverable

This is one of the most important factors to understand before committing.

Potentially Higher Overall Cost

In some cases, contract for deed can result in a higher overall cost compared to traditional financing.

This may happen due to:

- Higher interest rates

- Different pricing structures

- Additional fees built into the agreement

While not always the case, buyers should compare the total cost of the deal—not just the monthly payment.

Who May Benefit Most

Contract for deed is not for everyone, but it can be a strong fit for certain buyer profiles.

It may benefit buyers who:

- Have stable income but cannot qualify for a mortgage yet

- Are actively improving their credit situation

- Have some savings for a down payment

- Are comfortable committing to structured payments

These buyers are typically in a transitional stage where traditional financing is not currently available, but ownership is still a realistic goal.

Who Should Be More Cautious

Some buyers should approach contract for deed more carefully or consider alternatives.

This includes buyers who:

- Do not have stable or predictable income

- Are unsure about long-term commitment to the property

- Have not fully reviewed or understood the contract terms

- Are comparing options without understanding the differences

For these buyers, rushing into a contract for deed agreement can create more risk than benefit.

In many cases, it may be worth comparing other options or evaluating whether this path truly fits their situation.

How to Lower the Risks Before Signing

While contract for deed carries risk, there are practical steps buyers can take to reduce exposure and make more informed decisions.

1. Review the contract carefully

Understand all terms, including payment obligations, default conditions, and final transfer requirements.

2. Clarify all responsibilities

Know who is responsible for taxes, insurance, repairs, and maintenance.

3. Understand cancellation terms

Be clear on what happens if payments are missed and what options exist to resolve issues.

4. Compare total cost, not just monthly payment

Evaluate the full financial impact over time.

5. Avoid rushing into agreements

Take time to evaluate the deal and ensure it aligns with your long-term goals.

These steps do not eliminate risk entirely, but they significantly improve the chances of making a sound decision.

FAQs

What are the main pros of contract for deed in Minnesota?

The main advantages include flexibility, faster transactions, and access to homeownership for buyers who may not qualify for traditional financing.

What are the biggest risks of contract for deed?

The biggest risks include potential loss of the property if terms are not met, variability in contract terms, and delayed transfer of full ownership.

Is contract for deed a good idea in Minnesota?

It can be a good option for certain buyers, particularly those who are financially stable but not mortgage-ready. However, it depends heavily on the specific contract and the buyer’s situation.

Can you lose money with contract for deed?

Yes. If the contract is canceled or terms are not fulfilled, the buyer may lose payments made toward the property.

How can buyers protect themselves?

By reviewing the contract carefully, understanding all obligations, and making sure the agreement is realistic and manageable.