Welcome to Contract for Deed Guys in Minnesota

Missing a payment on a contract for deed is one of the most stressful situations a buyer can face. Whether it is a temporary setback or something more serious, most buyers in that moment want the same thing: a clear, honest answer about what happens next.

We have worked with a lot of Minnesota buyers over the years here at Contract For Deed Guys, and this question comes up more than people might expect — sometimes before signing, sometimes after a rough month. The honest answer is that the consequences can be significant, which is exactly why understanding them matters before you are in that situation, not after.

This article walks through what default means in a Minnesota contract for deed, how the process typically unfolds, what buyers stand to lose, and what you can do right now whether you are preparing to sign or already concerned about falling behind.

What Default Means in a Minnesota Contract for Deed

In a contract for deed arrangement, the buyer and seller agree to a set of terms in writing. The buyer makes monthly payments directly to the seller, lives in the property, and works toward eventual ownership. Default occurs when the buyer fails to meet one or more of those agreed terms — most commonly by missing payments.

Unlike a traditional mortgage, where a bank manages the process with its own legal team and servicing procedures, a contract for deed puts the seller in a more direct position. When a buyer defaults, the seller has the ability to act, and the Minnesota contract for deed law gives them a defined process to do so.

The specific consequences depend on what the written agreement says and how far the situation has progressed. But the general direction is consistent: missed payments trigger a notice process, and that notice process can lead to cancellation of the contract.

What Usually Happens After a Buyer Defaults

The process does not typically jump straight to the worst outcome. It tends to unfold in stages, and understanding those stages can help buyers respond in time.

The Missed Payment Stage

One missed payment rarely triggers immediate legal action. What it usually does is put the seller on alert. Depending on the relationship and the terms in the contract, a seller may reach out directly, apply a late fee as specified in the agreement, or simply begin documenting the situation.

What we have seen from experience is that buyers who communicate early — even just to explain a temporary hardship — tend to have more options than those who go quiet. Sellers are people too, and many would rather work something out than go through a legal process. That said, not every seller will feel that way, and the contract is ultimately what controls.

The Notice Stage

If payments remain missed or the buyer does not respond, the seller can move to formally notify the buyer of default under Minnesota law. Minnesota Statute § 559.21 governs the cancellation of contracts for deed, and it sets out a specific notice process that sellers must follow.

This notice is not informal. It is a legal document, and it starts a clock. Once a proper cancellation notice has been served, the buyer has a defined window to respond — either by curing the default (paying what is owed plus any required costs) or by facing the next stage.

The length of that window can vary depending on how the contract is written and the specific circumstances involved. This is one of the reasons why having a clear understanding of your contract’s default and cure language before signing is so important.

The Cancellation Risk Stage

If the buyer does not cure the default within the required period after receiving proper notice, the contract can be cancelled. At that point, the buyer’s rights under the agreement are terminated, and the seller may reclaim possession of the property.

This is where the situation becomes most serious.

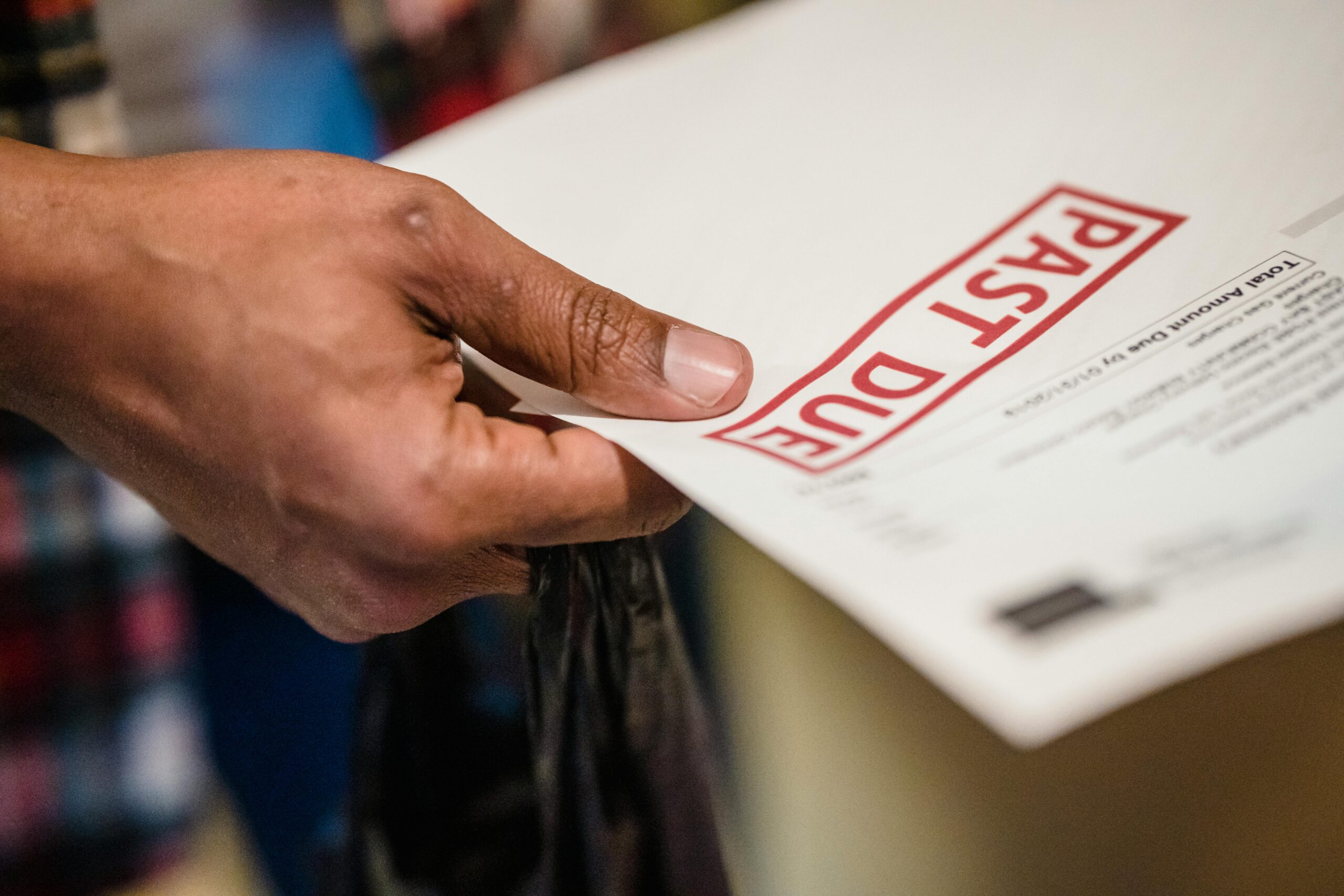

What Buyers May Lose if They Default

This is the part of the conversation that no one enjoys, but it is the part that matters most. A buyer who loses a contract for deed through default can face significant financial and practical consequences.

Possession of the Home

The most immediate risk is losing the right to live in the property. If the contract is cancelled and the buyer does not vacate voluntarily, the seller may pursue legal remedies to recover possession.

Money Already Paid

This is often the hardest part. In most contract for deed arrangements, payments made prior to cancellation are not automatically returned. Depending on how the contract is written, the buyer may lose the down payment and some or all of the monthly payments made over the course of the agreement.

This is one of the clearest reasons why affordability needs to be realistic from day one. A deal that stretches a buyer too thin is a deal that carries real financial risk beyond just the home itself.

The Opportunity to Cure

Whether a buyer has the right to cure a default — and for how long — depends on the specific terms of the agreement and applicable law. Minnesota does provide some protections in the cancellation process, but the specifics matter enormously. Buyers who are facing default should not assume they automatically have a long window to fix the problem.

Getting legal guidance at this stage is not optional. It is necessary.

What Buyers Should Do Immediately

If you are behind on payments or believe you are approaching default, the worst thing you can do is wait and hope the situation resolves itself.

Review the contract first. Pull out the signed agreement and read the default, notice, and cure sections carefully. Understand exactly what triggers default under your specific terms, what notice looks like, and what window you may have to respond.

Document all communication. Keep records of every conversation with the seller — text messages, emails, any written notices. If things escalate, documentation of what was said and when can matter.

Respond to the seller. If you have missed a payment and know why, reach out. A brief, honest explanation is not weakness. It is communication, and it sometimes leads to a short-term arrangement that keeps things from spiraling. Sellers do not always want to go through a cancellation process either.

Get legal help. If you have received a formal default notice, contact a Minnesota real estate attorney promptly. This is not the time for guesswork. The timelines in the cancellation process are real, and missing them has consequences.

How to Reduce the Risk of Default Before Signing

The best protection against default is building the right foundation before you ever sign anything.

One thing we consistently see at Contract For Deed Guys is that buyers who run into trouble later often knew, at some level, that the payment was going to be a stretch. The math felt close at the start, and then one unexpected expense changed everything.

Honest affordability review is not a hurdle — it is protection. If the monthly payment does not fit comfortably within your current income picture, that is important information. A deal that looks possible on paper but leaves no margin for real life is a deal worth pausing on.

Beyond affordability, a few practical habits significantly reduce default risk:

- Read the full contract before signing. Not just the payment amount. Read the default language, the notice language, the cure provisions, and what happens to payments you have made if things go wrong.

- Understand all costs, not just the monthly payment. Taxes, insurance, maintenance, and repairs are real costs. Know who is responsible for what before you move in.

- Keep a financial cushion if possible. Even a modest reserve can get a buyer through a rough month without defaulting.

- Communicate early if something changes. A job transition, a medical expense, a family situation — these things happen. Sellers who are notified early often have more flexibility than sellers who receive silence and then a missed payment.

Frequently Asked Questions

What happens if I miss one payment on a contract for deed in Minnesota? A single missed payment typically triggers a late fee if specified in the contract and may prompt communication from the seller. It does not immediately start the legal cancellation process, but it is a signal to act quickly — either by making the payment or reaching out to the seller to explain the situation.

Can I lose all the money I paid into a contract for deed if I default? Potentially, yes. In most cases, payments made before cancellation are not returned. The specific contract terms determine what happens, which is why understanding those terms before signing is so important.

How long do I have to cure a default in Minnesota? The timeframe depends on the terms of your contract and the applicable statutory process under Minnesota Statute § 559.21. There is no single universal window. If you have received a cancellation notice, contact a Minnesota real estate attorney immediately to understand your specific timeline.

Can I negotiate with the seller if I am behind on payments? Yes, and in many cases, it is worth trying. Sellers do not always prefer to go through a full cancellation process. If you are behind and can communicate a realistic plan, some sellers are willing to work out a short-term arrangement. There are no guarantees, but the conversation is almost always worth having.

Is default the same as foreclosure in Minnesota? No. Contract for deed cancellation and mortgage foreclosure are different legal processes. Foreclosure involves a lender and a mortgage. Contract for deed cancellation involves the seller directly and follows the process outlined in Minnesota Statute § 559.21. Both can result in loss of the property, but the timelines, procedures, and protections differ.

A Final Word

Defaulting on a contract for deed in Minnesota is a serious situation — but it is not always the end of the road if it is caught early and handled carefully.

The buyers we have seen navigate difficult patches most successfully are the ones who read their contracts, stayed in communication, and asked for help before things got to the formal notice stage. The buyers who struggled most were the ones who assumed it would work itself out.

If you are researching this topic because you are thinking about entering a contract for deed, that instinct to understand the risks first is exactly right. Go in informed.